Travel insurance becomes mandatory when traveling to Georgia from 2026

According to the Georgian Tourism Law, travel medical insurance becomes mandatory for all foreign tourists entering the country.

New tax – will insurance become more expensive from 2026? What is important for residents to know?

From January 1, 2026, all non-life insurance companies operating in Lithuania will have to pay a 10% security contribution tax on the amount of insurance

Phones at the wheel: browsing is more dangerous than talking

Are you standing in a traffic jam or at a traffic light? Then you are participating in traffic – the Road Traffic Act prohibits taking

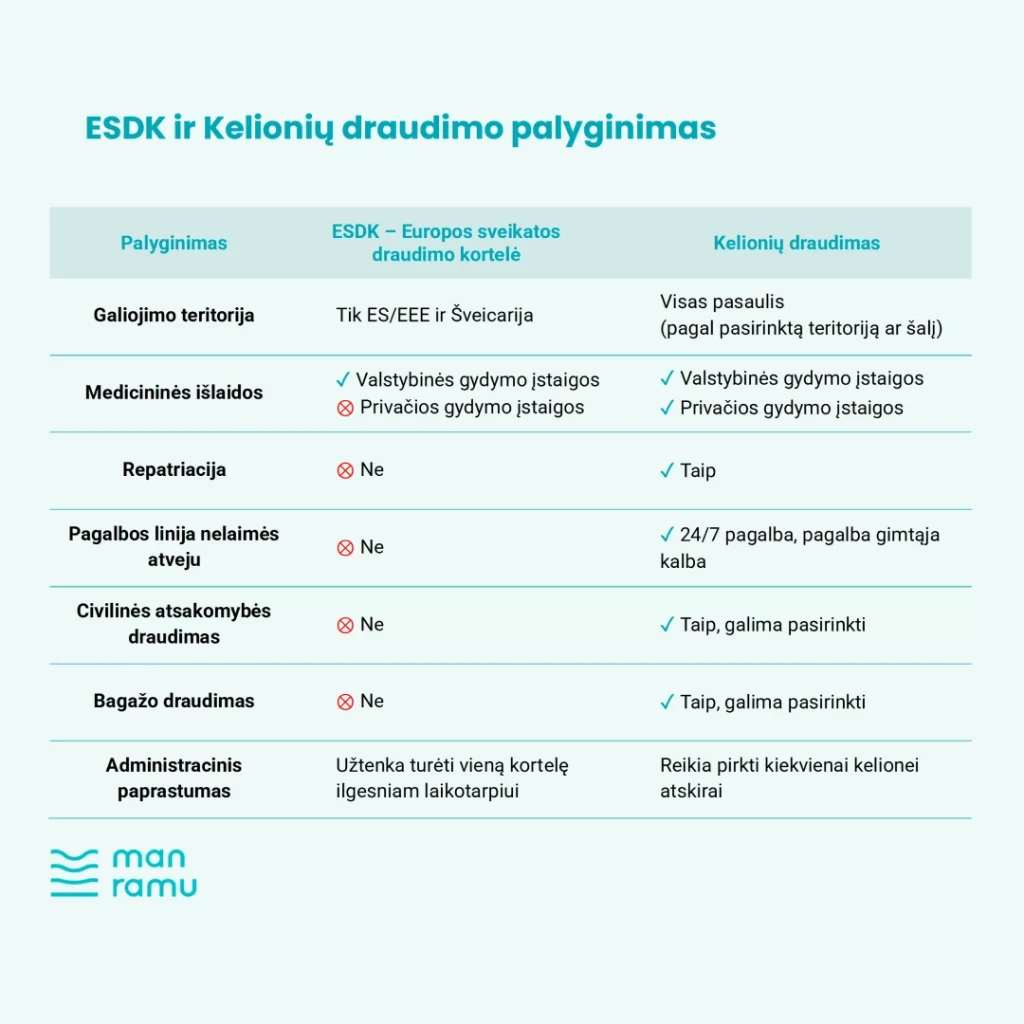

The European Health Insurance Card, often abbreviated as EHIC, is an official document issued to all citizens of the European Union, the EEA and

What to do if a son or daughter is about to drive their parents’ car? Find out when you need to rewrite your MTPL contract,

Drivers will be required to disclose whether a private car will be used for business activities

From 2026 When concluding a MTPL contract, private car owners will be required to confirm that they will not use the vehicle for economic activities.